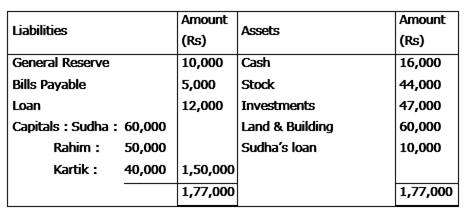

B and C were partners sharing profits in the ratio of 3 : 2. Their Balance Sheet as on 31-3-2011 was as follows:

|

Balance Sheet of B and C as on 31-3-2011 |

|

||||

|

Liabilities |

Amount Rs |

Assets |

Amount Rs |

||

|

Capital: |

|

|

Land and Building |

80,000 |

|

|

B |

60,000 |

|

Machinery |

20,000 |

|

|

C |

40,000 |

1,00,000 |

Furniture |

10,000 |

|

|

|

|

|

Debtors |

25,000 |

|

|

Provision for bad debts |

1,000 |

Cash |

16,000 |

||

|

Creditors |

|

60,000 |

Profit and Loss Account |

10,000 |

|

|

|

|

|

|

|

|

|

|

1,61,000 |

|

1,61,000 |

||

|

|

|

|

|

||

D was admitted to the partnership for 1/5th share in the profits on the following terms:

(i) The new profit sharing ratio was decided as 2:2:1.

(ii) D will bring Rs 30,000 as his capital and Rs 15,000 for his share of goodwill.

(iii) Half of goodwill amount was withdrawn by the partner who sacrificed his share of profit in favour of D.

(iv) A provision of 5% for bad and doubtful debts was to be maintained.

(v) An item of Rs 500 included in Sundry Creditors was not likely to be paid.

(vi) An provision of Rs 800 was to be made for claims for damages against the firm.

After making the above adjustments the Capital Accounts of B and C were to be adjusted on the basis of D Capital. Actual cash was to be brought in or to be paid off as the case may be.

Prepare Revaluation Account, Partner’s Capital Accounts and Balance Sheet of the new firm.

Dr Revaluation a/c Cr

|

Particulars |

Amount (Rs) |

Particulars |

Amount(Rs) |

|

Provision for bad and doubtful debt 1250 Less Old provision 1000 Claim for damages |

250 800 |

Sundry creditors Loss transferred to partners’ capital a/c B 330 C 220 |

500

550

|

|

|

1050 |

|

1050 |

Partner’s capital a/c

|

Particulars |

B |

C |

D |

Particulars |

B |

C |

D |

|

Goodwill a/c Realisation a/c Profit and loss a/c Cash a/c (bf) Balance c/d |

7500 330

6000

1170

60,000

|

220

4000

60,000 |

30,000 |

By Balance b/d Cash a/c Premium for good will a/c

Cash a/c (bf) |

60,000

15,000

|

40,000

24220 |

30,000 |

|

|

75,000 |

64,220 |

30,000 |

|

75,000 |

64,220 |

30,000 |

Working note:

Old profit sharing ratio: 3:2

New profit sharing ratio: 2:2:1

Sacrificing ratio: B: 3/5-2/5=1/5

C: 2/5-2/5=0=1/5:0

Adjustment of capital:

D’s capital: 30000

Total capital =30000*5/1=150000

B’s capital= 150000*2/5=60000

C’s capital=150000*2/5=60000

Computation of cash balance

|

particulars |

Amount |

Particulars |

Amount |

|

Opening balance D’s capital a/c Premium a/c C’s capital a/c

|

16,000 30,000 15,000 24,220 |

B’s capital a/c (7500+1170)

Balance c/d |

8670

76,550 |

|

|

85,220 |

|

85,220 |

|

Balance Sheet |

|||||

|

Liabilities |

Amount Rs |

Assets |

Amount Rs |

||

|

Capital: |

|

Land and Building |

80,000 |

||

|

B |

60,000 |

|

Machinery |

20,000 |

|

|

C |

60,000 |

|

Furniture |

10,000 |

|

|

D |

30,000 |

1,50,000 |

Debtors |

25,000 |

|

|

Creditors (60,000 – 500) |

59,500 |

Less: Provision for Doubtful Debts |

(1,250) |

23,750 |

|

|

Claim for Damages |

800 |

Cash |

76,550 |

||

|

|

|

|

|

||

|

|

|

|

|

||

|

|

|

|

|

||

|

|

2,10,300 |

|

2,10,300 |

||

|

|

|

||||