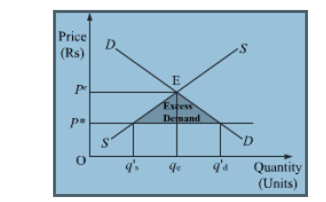

Explain the effects of 'maximum price ceiling' on the market of a good'? Use diagram.

A price ceiling is a government-imposed price control or limit on how high a price is charged for a product. Governments intend price ceilings to protect consumers from conditions that could make necessary commodities unattainable. It is the legislated or government imposed maximum level of price that can be charged by the seller. Since price ceiling is lower than the equilibrium price thus the imposition of the price ceiling leads to excess demand as shown in the diagram below.

The following are the consequences and effects of price ceiling:

1) An effective price ceiling will lower the price of a good, which decreases the producer surplus. The effective price ceiling will also decrease the price for consumers,but any benefit gained from that will be minimized by the decreased sales due to the drop in supply caused by the lower price.

2) If a ceiling is to be imposed for a long period of time, a government may need to ration the good to ensure availability for the greatest number of consumers.

3) Prolonged shortages caused by price ceilings can create black markets for that good.

4) Due to artificially lowering the price, the demand becomes comparatively higher than the supply. This leads to the emergence of the problem of excess demand.

5) The imposition of the price ceiling ensures the access of the necessity goods within the reach of the poor people. This safeguards and enhances the welfare of the poor and vulnerable sections of the society.

6) Each consumer gets a fixed quantity of good (as per the quota). The quantity often falls short of meeting the individual’s requirements. This further leads to the problem of shortage and the consumer remains unsatisfied.

7) Often it has been found that the goods that are available at the ration shops are usually inferior goods and are adulterated and infiltrated.