Sponsor Area

Market Equilibrium

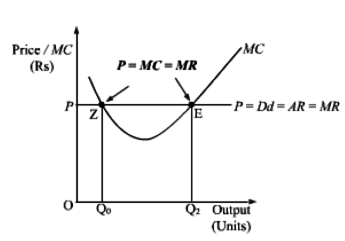

Why is the equality between marginal cost and marginal revenue necessary for a firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain.

Equilibrium refers to a state of rest when no change is required. A firm (producer) is said to be in equilibrium when it has no inclination to expand or to contract its output. This state either reflects maximum profits or minimum losses.

According to MC=MR approach, As long as MC is less than MR, it is profitable for the producer to go on producing more because it adds to its profits. He stops producing more only when MC becomes equal to MR.

When MC is greater than MR after equilibrium, it means producing more will lead to decline

in profits.

Both the conditions are needed for Firm’s Equilibrium:

1. MC = MR:

MR is the addition to TR from sale of one more unit of output and MC is addition to TC for

increasing production by one unit. Every producer aims to maximize the total profits. For

this, a firm compares it’s MR with its MC. Profits will increase as long as MR exceeds MC

and profits will fall if MR is less than MC. So, equilibrium is not achieved when MC < MR

as it is possible to add to profits by producing more. Producer is also not in equilibrium

when MC > MR because benefit is less than the cost. It means, the firm will be at

equilibrium when MC = MR.

2. MC is greater than MR after MC = MR output level:

MC = MR is a necessary condition, but not sufficient enough to ensure equilibrium. Only

that output level is the equilibrium output when MC becomes greater than MR after the

equilibrium.

It is because if MC is greater than MR, then producing beyond MC = MR output will reduce

profits. On the other hand, if MC is less than MR beyond MC = MR output, it is possible to

add to profits by producing more. So, first condition must be supplemented with the

second condition to attain the producer’s equilibrium.

Some More Questions From Market Equilibrium Chapter

Market for a good is in equilibrium. There is simultaneous decrease both in demand and supply of the good. Explain its effect on market price.

Market for a good is in equilibrium. There is an 'increase' in demand for this good. Explain the chain of effects of this change. Use diagram.

What is minimum price ceiling? Explain its implications.

If the prevailing market price is above the equilibrium price, explain its chain of effects.

The demand of a commodity when measured through the expenditure approach is inelastic. A fall in its price will result in :

(choose the correct alternative)

(a) no change in expenditure on it.

(b) increase in expenditure on it.

(c) decrease in expenditure on it.

(d) any one of the above

(choose the correct alternative)

(a) no change in expenditure on it.

(b) increase in expenditure on it.

(c) decrease in expenditure on it.

(d) any one of the above

As we move along a downward sloping straight line demand curve from left to right, price elasticity of demand : (choose the correct alternative)

(a) remains unchanged

(b) goes on falling

(c) goes on rising

(d) falls initially then rises

(a) remains unchanged

(b) goes on falling

(c) goes on rising

(d) falls initially then rises

Define market demand.

Show that demand of a commodity is inversely related to its price.

Explain with the help of utility analysis.

Or

Why is an indifference curve negatively sloped? Explain.

Explain with the help of utility analysis.

Or

Why is an indifference curve negatively sloped? Explain.

When price of a commodity X falls by 10 per cent, its demand rises from 150 units to 180 units. Calculate its price elasticity of demand. How much should be the percentage fall in its price so that its demand rises from 150 to 210 units ?

Complete the following table :

output units

total cost

average variable cost

marginal cost

average fixed cost

0

30

1

20

2

68

3

84

18

4

18

5

125

19

6

Sponsor Area

Mock Test Series

Mock Test Series