NCERT Classes

Previous Year Papers

Entrance Exams

State Boards

Home > NCERT Solutions > Mizoram Board > Class 12 > Accountancy > Accountancy Part Ii > Chapter 3 Financial Statements Of A Company

Sponsor Area

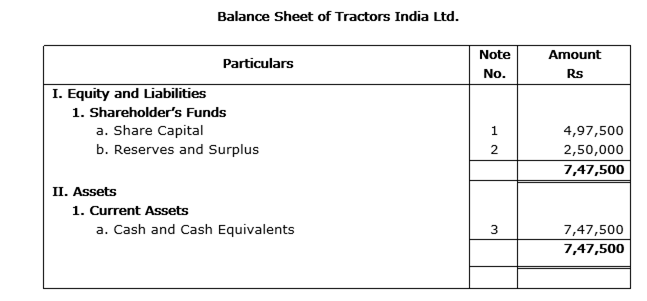

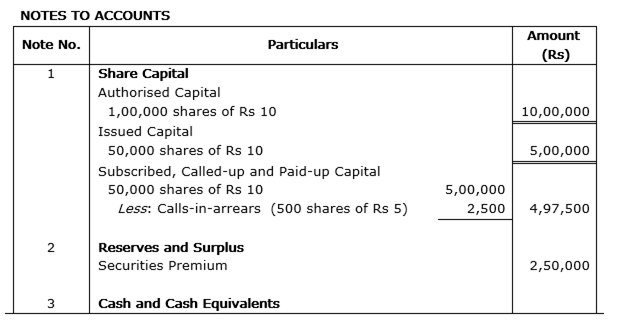

'Tractors India Ltd.' is registered with an authorized capital of Rs 10,00,000 divided into 1,00,000 equity shares of Rs 10 each. The company issued 50,000 equity shares at a premium of Rs 5 per share. Rs 2 per share were payable with application, Rs 8 per share including premium on allotment and the balance amount on first and final call. The issue was fully subscribed and all the amount due was received except the first and final call money on 500 shares allotted to Balaram.

Present the 'Share Capital' in the Balance Sheet of 'Tractors India Ltd.' as per Schedule VI Part I of the Companies Act, 1956. Also prepare Notes to Accounts for the same.

Under which major headings the following items will be presented in the Balance sheet of a company as per Schedule VI Part I of the Companies Act, 1956?(i) Loans provided repayable on demand(ii) Goodwill(iii) Copyrights(iv) Loose tools(v) Cheques(vi) General Reserve(vii) Stock of finished goods and(viii) 9% Debentures repayable after three years

Under which major sub-headings the following items will be placed in the Balance Sheet of a company as per revised Schedule-VI, Part-I of the Companies Act, 1956:(i) Accrued Incomes(ii) Loose Tools(iii) Provision for employees benefits(iv) Unpaid dividend(v) Short-term loans(vi) Long-term loans.

The authorized capital of Suhani Ltd. is Rs. 45,00,000 divided into 30,000 shares of Rs. 150 each. Out of these company issued 15,000 shares of Rs. 150 each at a premium of Rs. 10 per share.The amount was payable as follows:Rs. 50 per share on application, Rs 40 per share on allotment (including premium), Rs. 30 per share on first call and balance on final call. Public applied for 14,000 shares. All the money was duly received.Prepare an extract of Balance Sheet of Suhani Ltd. as per Revised Schedule VI Part I of the Companies Act 1956 disclosing the above information. Also prepare notes to accounts for the same.

Under which heads and sub-heads the following items will appear in the Balance Sheet of a company as per revised Schedule VI, Part-I of the Companies Act 1956. i. Premium on Redemption of Debenturesii. Loose Toolsiii. Balance with Banks

List the items which are shown under the heading current liabilities and provisions as per Schedule VI Part-I of the Companies' Act, 1956.

One of the objectives of ‘Financial Statements Analysis’ is to identify the reasons for the change in the financial position of the enterprise, State two more objectives of this analysis.

Name any two items that are shown under the head’ Other Current Liabilities’ and any two items that are shown under the head ‘Other Current Assets’ in the Balance Sheet of a company as per schedule III of the Companies Act, 2013

Following is the statement of Profit and Loss of Sun India Ltd. For the year ended 31st March. 2015:The motto of Sun India Ltd is to produce and supply green energy in the rural areas of India. It has also taken up a project of constructing a road that will pass through five villages so that these villages could be connected to the nearby town. It will use the local resources and employ local people for construction of the road. You are required to prepare a Comparative Statement of Profit and Loss of Sun India Ltd from the given statement of Profit and Loss. Also, identify any two values that the company wishes to convey to the society

Financial Statements are prepared following the constituent accounting concepts principles procedures and also the legal environment in which the business organisationoperate. These statements are the source of information on the basis of which conclusions are drawn about the profitability and financial position of acompany so that their users can easily understand and use them in their economic decisions in a meaningful way.

From the above statements identify any two values that a company should observe while preparing its financial statements. Also, State under which major headings and sub-headings the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act 2013.(i) Capital Reserve(ii) Calls-in-Advance(iii) Loose Tools(iv) Bank Overdraft

Mock Test Series