☰

Issue and Redemption of Debentures

Bharat Ltd. had an authorized capital of Rs 20,00,000 divided into 2,00,000 equity shares of Rs 10 each. The company issued 1,00,000 shares and the dividend paid per share was Rs 2 for the year ended 31-3-2008. The management of the company decided to export its products to the neighbouring countries Nepal, Bhutan, Sri Lanka and Bangladesh. To meet the requirement of additional funds the financial manager of the company put up the following three alternatives before its Board of Directors:

(i) Issue 54,000 equity shares

(ii) Obtain a loan from Import and Export Bank of India. The loan was available at 12% per annum interest.

(iii) To issue 9% Debentures at a discount of 10%.

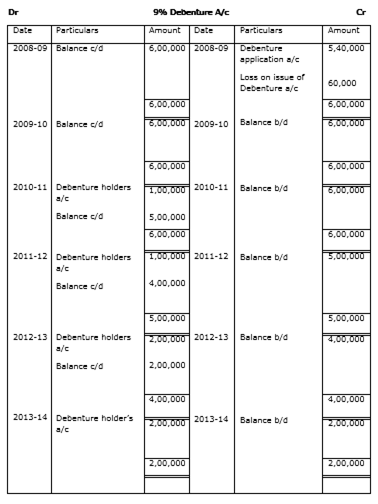

After comparing the available alternatives the company decided on 1-4-2008 to issue 6,000 9% debentures of Rs 100 each at a discount of 10%. These debentures were redeemable in four installments starting from the end of third year. The amount of debentures to be redeemed at the end of third, fourth, fifth and sixth year was as follows:

| Year | Profit Rs |

| III | 1,00,000 |

| IV | 1,00,000 |

| V | 2,00,000 |

| VI | 2,00,000 |

Prepare 9% Debentures Account for the year 2008-09 to 2013-14.

Sponsor Area

Pass necessary journal entries in the following cases:

(i) Z Ltd redeemed 1500, 12% debentures of Rs 100 each issued at a discount of 6% by converting them into equity shares of Rs 100 each issued at a premium of Rs 25 per share.

(ii) X Ltd. converted 1,000, 12% debentures of Rs 100 each issued at a discount of Rs 10 per debenture into equity shares of Rs 100 each Rs 90 paid up.

What is meant by issue of debentures as a collateral security?

Pass the necessary journal entries for issue of 1,000, 7% Debentures of Rs. 100 each in the following cases:

(a) Issued at 5% premium redeemable at a premium of 10%.

(b) Issued at a discount of 5% redeemable at par.

Taneja Constructions Ltd. has an outstanding balance of Rs. 5,00,000, 7% debentures of Rs. 100 each redeemable at a premium of 10%. According to the terms of redemption, the company redeemed 30% of the above debentures by converting them into shares of Rs. 50 each at a premium of 20%. Record the entries for redemption of debentures in the books of Taneja Constructions Ltd.

Give any one advantage for the redemption of debentures by purchase in the open market?

Narain Laxmi Ltd. invited applications for issuing 7500, 12% Debentures of Rs100 each at a premium of Rs 35 per Debenture. The full amount was payable on application.

Applications were received for 10,000 Debentures. Applications for 2500 Debentures were rejected and the application money was refunded. Debentures were allotted to the remaining applicants.

Pass necessary Journal Entries for the above transactions in the books of Narain Laxmi Ltd.

Pass necessary Journal Entries for the following transactions in the books of Sudarshan Ltd:

(i) Redeemed 750, 12% Debentures of Rs 75 each by converting into Equity Shares of Rs 100 each. The Equity Shares were issued at a discount of 10%.

(ii) Converted 550, 12% Debentures of Rs 1,000 each into New 13% Debentures of Rs 100 each. The New Debentures were issued at a premium of 10%.

Pass the necessary Journal entry when 10,000 debentures of Rs. 100 each are issued as collateral security against a Bank loan of Rs. 8,00,000.

X Ltd. redeemed 100, 6% Debentures of Rs. 100 each by converting them into Equity Shares of Rs. 100 each. The 6% Debentures were redeemable at 10% premium for which the Equity Shares were issued at 25% premium. Pass the necessary Journal entries for the redemption of above-mentioned debentures in the books of X Ltd.

On 1st April, 2008'a company made an issue of Rs. 2,00,000, 6% Debentures of Rs. 100 each, repayable at a premium of 10%. The terms of issue provided for the redemption of 400 debentures every year starting from the end of 31-3-2010 either by purchase from the open market or by draw of lots at the company's option.

On 31-3-2010, the company purchased for cancellation 300 Debentures at 95% and 100 Debentures at 90%.

Pass the necessary Journal entries for the issue and redemption of debentures assuming that the company had already created the Debenture Redemption Reserve A/c by the required amount.

Sponsor Area

Sponsor Area