Why is a production possibilities curve concave? Explain.

Production Possibility Curve (PPC) is concave to the origin because of the increasing opportunity cost. As we move down along the PPC, to produce each additional unit of one good, more and more units of other good need to be sacrificed. That is, as we move down along the PPC, the opportunity cost increases. And this causes the concave shape of PPC.

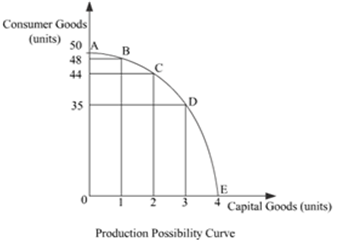

In the above graph, AE represents the PPC for capital goods and consumer goods. Suppose the initial production point is B, where 1 unit of capital goods and 48 units of consumer goods are produced. To produce one additional unit of capital good, 4 units of consumer good must be sacrificed (point c). Thus at point c, the opportunity cost of one additional capital good is 4 units of consumer goods. On the other hand, at point D, the opportunity cost of producing one additional unit of capital good is 9 units of consumer goods. Thus, as we move down the PPC from point C to point D, the opportunity cost increases. This confirms the concave shape of PPC.