Sponsor Area

Determination of Income and Employment

State briefly the Classical Theory and the Keynesian Theory of Income and Employment.

(a) Classical Theory of Employment. The classical economists believed that:

(i) An economy as a whole always functions at the level of full employment of resources. This belief is based on Say's Law of Market that states, 'Supply creates its own demand.” which implies that supply (production) creates a matching demand for it with the result that whole of it is sold out. Therefore, there is neither overproduction nor underproduction.

Thus full employment is a normal situation and if at all there arises any unemployment, it is automatically corrected by market forces. Hence equilibrium level of income occurs at level of full employment, i.e., there is always full employment equilibrium. Therefore, Classicals advocated for a free economy.

(ii) Flexibility of prices and wages. Even if at any time there is unemployment, it must be temporary because in a free economy, flexibility of prices and wages automatically bring about full employment. Suppose at a given wage rate there is unemployment which implies that supply of labour is greater than demand for it. Competition among labour to seek employment would lead to fall in wage rate. As a result demand for labour would continue to rise until unemployment is removed from the labour market. Thus wage-price flexibility is the built-in stabiliser to ensure full employment.

The Great Depression of 1929–33. During 1929-33 there was a world-wide depression. Fall in aggregate demand was so severe that investment came down to its minimum level resulting in vast unemployment. This situation which brought great disaster to U.S.A. and other European countries fully exploded the Classical's myth that there is always tendency of full employment equilibrium. The Great Depression led to break down of Classical theory.

It was at that time that J.M. Keynes, a British Economist propounded his own theory and in 1936 brought out his famous book, 'General Theory of Employment, Interest and Money,' which brought about a revolution in economic thought. This led to emergence of Macroeconomics as a separate branch of economics.

(b) Keynesian Theory of Income and Employment. According to Keynes:

(i) An economy can be in equilibrium at less than full employment level Economic system does not ensure automatic equilibrium at full employment as believed by Classicals. There can be equilibrium (equality between aggregate demand and aggregate supply) even at less than full employment level whereas according to Classicals equilibrium is always at full employment. Thus there is divergence between the point of equilibrium attained by an economy and the point of equilibrium at which an economy has full employment of resources. This is the basic difference between Classical Theory and Keynesian Theory.

(ii) 'Demand creates its own supply' Unlike Classicals; Keynes believed that it is the demand that creates supply and not that supply creates demand. In fact, aggregate demand in the economy is the driving force that determines the level of output, employment and income. It is because the level of aggregate supply is constant during short period. If aggregate demand increases, level of output will increase to meet the increased demand. As a result, employment and income will also rise. Thus increase in demand has led to increase in output, employment and income.

This is the gist of Keynesian or Macro approach. The scope of this chapter is limited to Keynesian Theory. The core issue of macroeconomics is the determination of level of income, employment and output. According to this theory, in an economy income and employment are in equilibrium at the level at which Aggregate Demand (AD) = Aggregate Supply (AS). It needs to be noted that Keynesian theory is supposed to apply under short run and perfect competition. Since during short period supply is constant, it is because of deficiency in effective demand, which causes unemployment. So aggregate demand should be raised in order to raise level of employment. Let us, therefore, start with the meaning of aggregate demand (AD).

What do you understand by aggregate demand (AD)?

Aggregate demand broadly refers to the total demand for final goods and services in the economy. Since it is measured by total expenditure of the community on goods and services, therefore, aggregate demand also means aggregate expenditure on final goods and services in the economy. In other words, AD is the total expenditure which all sectors of economy are willing to make on purchase of goods and services. Thus aggregate demand is synonymous with aggregate expenditure in the economy. Mind, determination of output and employment in Keynesian framework depends mainly on level of aggregate demand in short period.

Explain the meaning of aggregate supply (AS).

Aggregate supply is the money value of total output available in the economy for purchase during a given period. When expressed in physical terms, aggregate supply refers to the total output of goods and services produced for sale by all the entrepreneurs in an economy. It is assumed that in short-run, prices of goods do not change and elasticity of supply is infinite. At the given price level, output can be increased till all the resources are fully employed.

If we go deep, we will find aggregate supply is represented by national income. How? We know that money value of final output is distributed as rent, wages interest and profit among factors of production who help produce the output. Since sum of factor incomes (rent, wages, interest and profit) at national level is called national income, therefore, aggregate supply, output and national income are same. Alternatively AS = Y where Y is national income. Thus income or total output measures the aggregate supply of goods and services.

Aggregate Supply = Output = Income

A major portion of income is spent on consumption of goods and services and the balance is saved. Thus national income or aggregate supply (AS) is sum of consumption expenditure (C) and savings (S). Put in the form of an equation:

AS = C + S

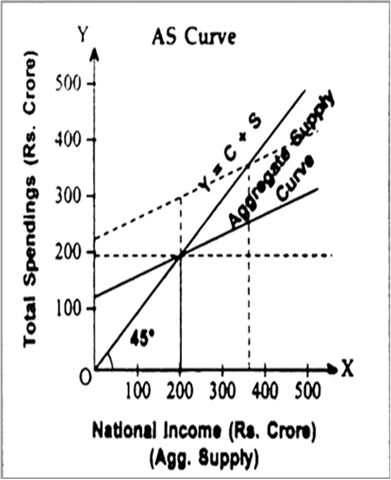

Clearly aggregate supply has two components, namely, consumption expenditure and savings. AS curve is depicted in the adjoining Fig.(a) Aggregate supply or national income is shown on X-axis and total spending (consumption + savings) on Y-axis.

AS curve is shown by a 45° line from the origin. Why? Its significance is that every point on this line is equidistant from X-axis and Y-axis taking same scale on both the axes, i.e., at each point on this line, Expenditure (AD) = Income (AS,). Thus 45° line (also called a Guideline) helps us to identify equilibrium when two variables are to be shown graphically equal,

(Classical and Keynesian concepts of Aggregate Supply. There is difference between these two concepts. According to Classicals "Aggregate supply is perfectly inelastic with respect to prices and it (aggregate supply) is always at full employment level of output." According to Keynes "Aggregate supply is perfectly elastic with respect to prices till the full employment level of output is reached.").

Fig.(a)

What is meant by Propensity to consume (or Consumption function)?

Meaning of Consumption Function. Consumption function shows the mathematical relation between income and consumption i.e. how much of income is spent on consumption goods. Simply put, consumption function (or Propensity to consume) means proportion of income spent on consumption. Its two features are noteworthy. (i) At zero or very low level of income, consumption expenditure is higher than income because minimum consumption is necessary for survival, and (ii) As income increases, consumption expenditure also increases but increase in consumption is less than the increase in income. Mind, level of household consumption depends directly on the level of income. Thus consumption (C) is a function (f) of income. Symbolically: C = f(Y).

Consumption function (linear, i.e., straight line consumption function) is represented by the following equation.![]()

Thus total consumption (C) comprises two components (i) Autonomous Consumption  not influenced by income, and (ii) Induced Consumption (bY) influenced by income. For example, the consumption equation C = 30 + 0.75 Y means र 30 is autonomous consumption which is incurred without having any income. As income increases, 75% of additional income is spent on consumption. In short, consumption equation

not influenced by income, and (ii) Induced Consumption (bY) influenced by income. For example, the consumption equation C = 30 + 0.75 Y means र 30 is autonomous consumption which is incurred without having any income. As income increases, 75% of additional income is spent on consumption. In short, consumption equation  shows that Consumption (C) at a given level of income (Y) is equal to autonomous consumption

shows that Consumption (C) at a given level of income (Y) is equal to autonomous consumption  times of given level of income. Some numericals for further clarification are given below.

times of given level of income. Some numericals for further clarification are given below.

Sponsor Area

Mock Test Series

Mock Test Series