Sponsor Area

Accounting for Partnership:Basic Concepts

In the absence of partnership deed the profits of a firm are divided among the partners:

(a) In the ratio of capital

(b) Equally

(c) In the ratio of time devoted for the firm's business

(d) According to the managerial abilities of the partners

(b) Equally: According to partnership act 1932, in the absence of any partnership deed, profits of the firm are divided among the partners equally.

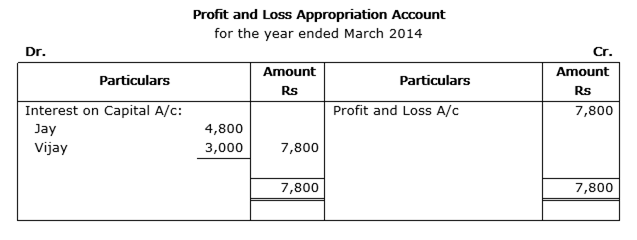

On 1-4-2013 Jay and Vijay, entered into partnership for supplying laboratory equipment’s to government schools situated in remote and backward areas. They contributed capitals of Rs 80,000 and Rs 50,000 respectively and agreed to share the profits in the ratio 3: 2. The partnership deed provided that interest on capital shall be allowed at 9% per annum. During the year the firm earned a profit of Rs 7,800.

Showing your calculations clearly, prepare 'Profit and Loss Appropriation Account' of Jay and Vijay for the year ended 31-3-2014.

Working Notes:

Calculation of Interest on Capital

Interest on Jay’s capital = 80000*9/100=7200 Rs

Interest on Vijay’s capital = 50,000*9/100 = 4500 Rs

Total interest = 7200+4500 = Rs 11,700

Calculation of proportionate Interest on capital

Jay: (7200/11700)*7800 = Rs 4800

Vijay: (4500/11700) * 7800 = Rs 3000

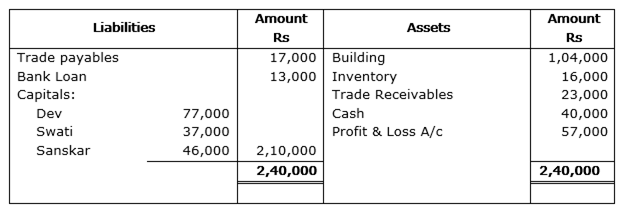

Dev, Swati and Sanskar were partners in a firm sharing profits in the ratio of 2:2:1. On 31-3-2014 their Balance Sheet was as follows:

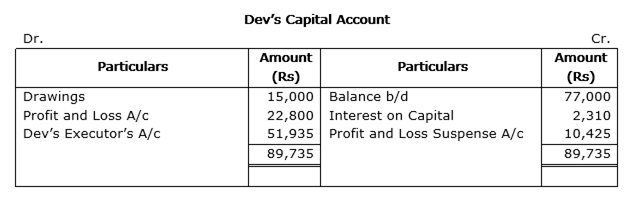

On 30thJune, 2014 Dev died. According to partnership agreement Dev was entitled to interest on capital at 12% per annum. His share of profit till the date of his death was to be calculated on the basis of the average profits of last four years. The profit of the last four years were:

| Years | Profit (RS) |

| 2010-2011 | 2,04,000 |

| 2011-2012 | 1,80,000 |

| 2012-2013 | 90,000 |

| 2013-2014(Loss) | 57,000 |

On 1-4-2014, Dev withdrew Rs 15,000 to pay for his medical bills.

Prepare Dev's account to be presented to his executors.

Working Notes:

Calculation of Interest on Capital:

77,000*12/100*3/12 = 2310 Rs

Calculation of Share of Profit:

Average Profit = (2,04,000+1,80,000+90,000-57,000)/4 = 1,04,250 Rs

Dev’s share of profit = 1,04,250*3/12*2/5 = Rs 10,425

Calculation of Share of Debit balance in P&L A/c

57,000*2/5 = Rs 22,800.

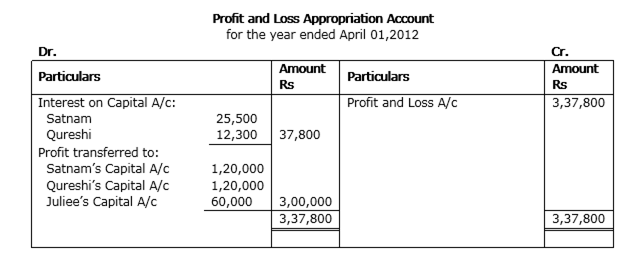

Satnam and Qureshi after doing their MBA decided to start a partnership firm to manufacture ISI marked electronic goods for economically weaker section of the society. Satnam also expressed his willingness to admit Juliee as partner without capital who is especially abled but a very creative and intelligent friend of him. Qureshi agreed to this. They formed a partnership on 1st April 2012 on the following terms:

(i) Satnam will contribute Rs 4,00,000 and Qureshi will contribute Rs 2,00,000 as capitals.

(ii) Satnam, Qureshi and Juliee will share profits in the ratio of 2:2:1.

(iii) Interest on capital will be allowed @ 6% p.a. Due to shortage of capital Satnam contributed Rs 50,000 on 30th September, 2012 and Qureshi contributed Rs 20,000 on 1st January, 2013 as additional capitals. The profit of the firm for the year ended 31st March, 2013 was Rs 3,37,800.

(a) Identify any two values which the firm wants to communicate to the society.

(b) Prepare Profit & Loss Appropriation Account for the year ending 31st March, 2013.

(a) Values:

1) Devotion to law, to manufacture ISI marked goods.

2) Sensitivity towards especially abled people.

(b)

Working Notes:

Calculation of Interest on Capital:

a) Interest on Satnam’s capital:

On Initial capital of Rs 4,00,000

4,00,000* 6% = 24,000

On additional capital of Rs 50,000

50,000* 6% * 6/12 = 1500

Total interest on Satnam’s capital = 24000 + 1500 = Rs 25,500.

b) Interest on Qureshi’s Capital:

On initial capital of Rs 2,00,000

2,00,000* 6% = Rs 12,000

On additional capital of Rs 20,000

20,000 * 6% * 3/12 = Rs 300

Total interest on Qureshi’s Capital = 12,300

Sponsor Area

Mock Test Series

Mock Test Series