Sponsor Area

Accounting For Share Capital

Joy Ltd. issued 1,00,000 equity shares of Rs 10 each. The amount was payable as follows:

On application Rs 3 per share.

On allotment Rs 4 per share.

On 1st and final call balance.

Applications for 95,000 shares were received and shares were allotted to all the applicants. Sonam to whom 500 shares were allotted failed to pay allotment money and Gautam paid his entire amount due including the amount due on first and final call on the 750 shares allotted to him along with allotment. The amount received on allotment was

(a) Rs 3,80,000

(b) Rs 3,78,000

(c) Rs 3,80,250

(d) Rs 4,00,250

Amount received on allotment is option (c) Rs 3,80,250.

| Particulars | Amount (Rs.) |

Amount due on allotment (95000 * 4) Less: Allotment not received on 500 shares Add: First and Final call money received on 750 shares |

3,80,0000 2,000 2,250 |

| Net Amount Received on Allotment | 3,80,250 |

Give the meaning of forfeiture of shares.

Forfeiture of share means the cancellation of allotment due to breach of contract and to treat the amount already received on such shares as forfeited to the company.

State any three purposes other than 'issue of bonus shares' for which securities premium can be utilized.

The amount of securities premium can be utilised for the following purposes:

1) For writing-off the preliminary expenses of the company.

2) For writing-off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the company.

3) For paying up the premium payable on redemption of redeemable preference shares or debentures of the company.

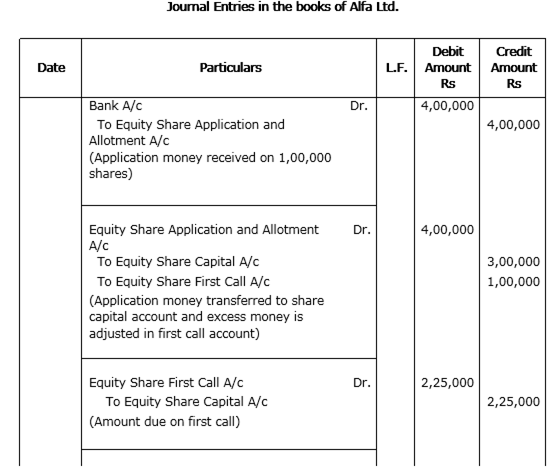

Alfa Ltd. invited applications for issuing 75,000 equity shares of Rs 10 each. The amount was payable as follows:

On application and allotment Rs 4 per share. On first call Rs 3 per share. On second and final call balance.

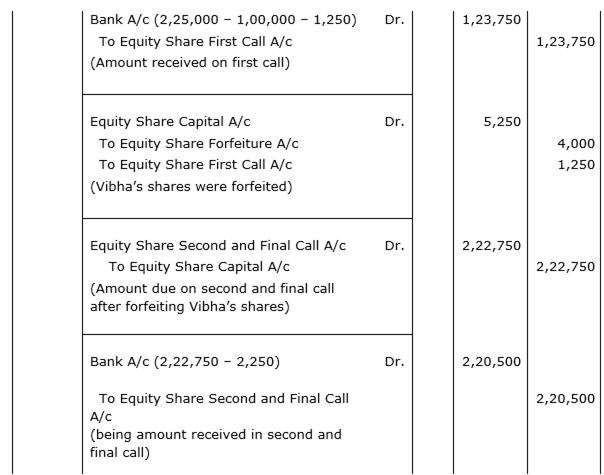

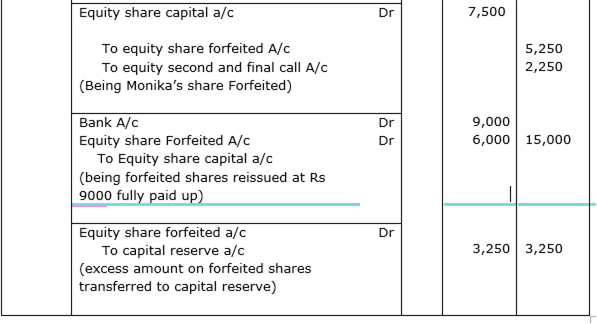

Application for 1,00,000 shares were received. Shares were allotted to all the applicants on pro-rata basis and excess money received with applications was transferred towards sums due on first call. Vibha who was allotted 750 shares failed to pay the first call. Her shares were immediately forfeited. Afterwards, the second call was made. The amount due on second call was also received except on 1000 shares, applied by Monika. Her shares were also forfeited. All the forfeited shares were re-issued to Mohit for Rs 9,000 as fully paid up.

Pass necessary journal entries in the books of Alfa Ltd. for the above transactions.

Working Note:

Calculation of amount not received on first call:

Shares applied by Vibha:

(1,00,000/75,000)* 750 = 1,000 shares

Amount received on 1,000 shares @ Rs 4 each = 4000 Rs

Amount transferred to share capital a/c (750*4) = 3000 Rs

Excess application and allotment money received = 1000 Rs

Amount due on first call @ Rs 3 each: 2250 Rs

Amount not received on first call = 1,250 Rs (2250-1000)

Calculation of amount not received on second call:

Shares allotted to Monika = (75,000/1,00,000)* 1000 = 750 shares

Amount not received on second call = Rs 2250 (750*3)

Sponsor Area

Mock Test Series

Mock Test Series